Artificial Intelligence Enthusiasm and Infrastructure Capex: The $400B+ Flywheel Driving Markets (and the Economy) Higher

As we approach the holiday season, AI enthusiasm continues to lift and support the equity markets. AI Infrastructure spending or “AI-related Capex” has doubled in the past two years and continues to accelerate. Core hyperscalers are on track for $400-$450B+ in AI-heavy capex in calendar/fiscal 2025, with guidance pointing to another larger step-up in 2026.

AI Ecosystem: Hardware Developers, Hyperscalers and AI Development Companies

Hardware Developers: Companies providing the equipment: building chips, processors, servers and networking equipment.

- Nvidia (NVDA)

- Advanced Micro Devices (AMD)

- Broadcom (AVGO)

- Oracle (ORCL) – increasingly a Hyperscaler peer.

Hyperscalers: Established companies with high free cash flow and capital to scale and integrate AI into their products. They provide compute power, cloud infrastructure, etc.

- Microsoft (MSFT)

- Amazon (AMZN)

- Google (GOOG/GOOGL)

- Meta/Facebook (META)

Private AI Labs/Development Companies: Companies where AI development is the core focus. They are buying the equipment and creating the AI models such as Chat GPT.

- OpenAI (privately owned)

- xAI (privately owned)

- Anthropic (privately owned)

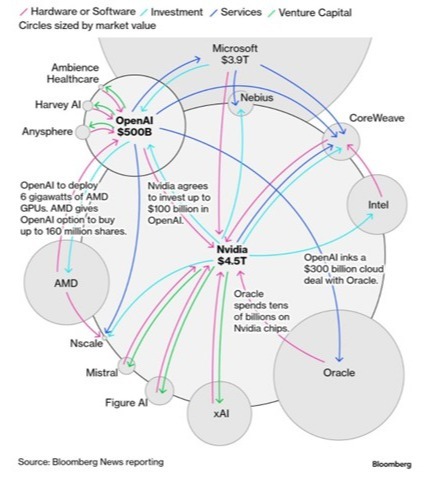

As new circular financing deals are being announced almost daily, the connectivity and scale of these deals has drawn attention and some scrutiny with many outlets highlighting this trend with the diagram below.

As long as there is economic viability to these deals and downstream demand materializes as expected by the participants, these circular financing agreements need not be troublesome. However, these arrangements are essentially vendor financing on steroids – healthy when demand is real (as it appears today), but they amplify the risk if utilization disappoints or power/grid constraints bite harder than expected.

Economic Impact

Accelerating AI capex is helping drive economic growth in the US, offsetting pressures created by tariff uncertainty, decelerating consumer spending growth, and a weakening labor market. As formerly asset-light companies race to build out infrastructure, AI capex spending in 2026 is projected to be 2-3X the capex levels for asset-heavy sectors like energy, industrials, and utilities. AI capex is now running at ~ 1.5-2.0% of U.S. GDP and contributed an estimated 0.7 -1.1 percentage points to real GDP growth thus far in 2025 – more than consumer spending added in some quarters. This highlights the importance of AI to future economic growth and suggests caution is warranted if signs of broken deals or meaningfully reduced future capex emerge.

Why it Matters

Valuations and concentration in the S&P 500 are undeniably elevated. But, the scale and profitability of the companies doing the majority of the spending (by pouring hundreds of billions into infrastructure because they believe there is massive downstream return on investment) certainly demonstrates their conviction and differentiates this cycle from the late 1990s – early 2000 tech bubble. Whether their conviction is warranted will ultimately have a significant impact on the economy and markets. As long as execution continues and utilization ramps, this capex flywheel should keep supporting both economic growth and equity markets.

Written by Your Planning Works Team